Central Banks around the world responded with unprecedented monetary and fiscal stimulus to support financial liquidity, companies and their employees, increasingly on a 'whatever it takes' basis.

Equity investors remain fearful of a severe and prolonged economic downturn, reflected in a weekly EUR fall of 11.7% for the MSCI World Index, which is now down 23.2% year-to-date.

Here are selected events relevant for our funds:

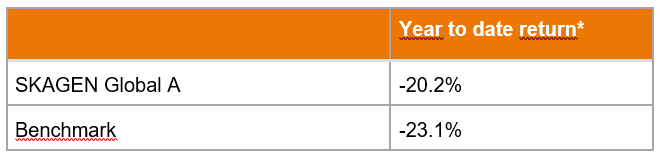

SKAGEN Global

- The portfolio managers continue to focus on bottom-up fundamental research on existing and prospective positions to selectively capitalise on excess volatility and improve the long-term outlook for the portfolio.

- The fund did not enter any new positions or exit any current holdings last week, making minor adjustments on extreme stock movements.

- The fund retains a liquid portfolio with a cash position below 1% in order to remain invested in the market.

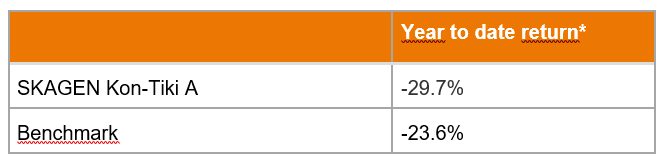

SKAGEN Kon-Tiki

- The fund had an active week from a trading perspective with five 'hot-pots' currently in progress. These are either relatively defensive companies or cyclicals with strong balance sheets to better weather a downturn in demand.

- The portfolio managers have also added to some of the fund's more defensive positions and carefully increased its quality exposure.

- Selling activity has generally been to re-balance the portfolio on the back of relative performance and fund flows. The fund managers have, however, reduced holdings in weaker cyclical companies and those with a higher combination of operational and financial leverage.

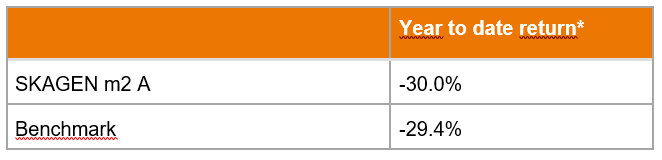

SKAGEN m2

- The investment team continues to focus on what they believe to be resilient sub-segments of the property market with strong cash flow generation and balance sheet structures. They continue to build positions in operationally and financially stable companies, selectively buying into new and existing quality names.

- With policymakers continuing to frantically fix leaks as they appear in the plumbing of the global financial system, the variables are inevitably impacting the valuation of real estate assets.

- The fallout from what threatens to be a record-breaking plunge in GDP should have predictable impacts across property sectors. The outlook is complicated, however, by outsized effects on properties that serve as gathering spots and / or cater to tourists or older people.

- Less clear is whether the market has discounted the impact that cash flow disruptions and excessive leverage might have on real estate companies with less-than-pristine balance sheets. Balance sheets have been easy to ignore in recent years, but they will likely serve as significant return differentiators going forward.

- The recent performance of listed real estate implies a significant decline in asset values that ranges widely across sectors. Research from NAREIT and other sources has demonstrated that 1) private and public real estate markets are inexorably linked over the long-run; and 2) buying listed real estate when it trades at a large discount to the underlying asset value is a recipe for outperformance. Public market volatility represents an opportunity long-term, rather than a threat.

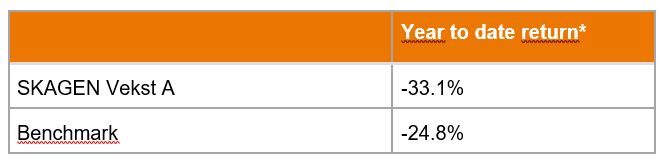

SKAGEN Vekst

The portfolio managers have focused on downside protection in case we experience a prolonged economic downturn, while still maintaining the fund's upside potential.

This has been implemented by reducing positions in companies with financial leverage while adding to companies with stronger balance sheets but more cyclically exposed revenues.

While Vekst has a few illiquid positions, the overall portfolio is very liquid and has 4% in cash.

SKAGEN Focus

- The portfolio managers believe the downturn will finally expose a large part of the 'quality/growth' complex, which still trades at exceptional multiples, as being more cyclical than previously perceived and will result in shrinking valuation multiples. This development could potentially gain further momentum from substantial outflows from index and ETF-related vehicles as retail investors finally capitulate, primarily in the US.

- The portfolio managers sense that the Korean and Japanese equities, with superior financial situations, solid balance sheets and net cash positions should produce substantial outperformance, which would benefit the fund on a relative basis given a third of assets are invested in highly undervalued Japanese and Korean equities with strong balance sheets.

- The portfolio's record low allocation to US-listed companies, currently 13.8%, could also deliver relative outperformance given the economy is heading for an extremely difficult period as the country faces an unprecedented shutdown to limit the effects of Covid-19.

- The fund has gradually initiated several new positions where the portfolio managers observe an exceptional risk/reward profile over 2-3 years.

- The fund's cash position was 7% at the end of the week.