Following the example of the US Federal Reserve, central banks have tried to limit the economic effects of the coronavirus crisis. Several have lowered interest rates, including the Bank of England and Norges Bank, both of which cut rates by 50bps. Other measures have been targeted to keep liquidity and credit flowing, including cheap loans to banks, quantitative easing and lower reserve requirements for banks. Governments are also initiating financial help and emergency packages.

The volatility in government bond and FX markets has also been extreme. Risk premiums increased and currencies depreciated everywhere not deemed to be a safe haven; even Germany and the US experienced very high volatility last week. Christine Lagarde's comment at the European Central Bank (ECB) press conference on Thursday that it is not the ECB's job to safeguard low credit spreads within the Eurozone led to a sharp increase in credit spreads from France to Greece (all relative to Germany). Emerging market currencies and interest rates have been hit particularly hard, as is always the case during periods of flight to safety.

Here are selected events relevant for our funds:

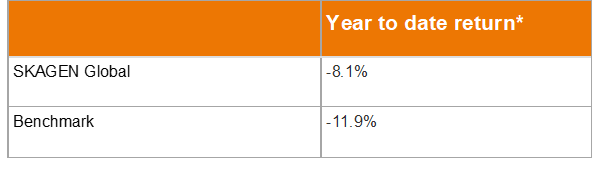

SKAGEN Global

- The portfolio managers continue to focus on bottom-up fundamental research of existing and prospective positions to selectively capitalise on excess volatility and improve the long-term outlook of the portfolio.

- Following the oil price collapse, the fund has re-entered the energy sector with a new position as the portfolio managers believe that oil in the region of USD 30 a barrel is beginning to tilt the risk-reward more favourably.

- The fund has a low cash position in order to remain fully invested in the market. Nonetheless, SKAGEN Global has a liquid and well-diversified portfolio.

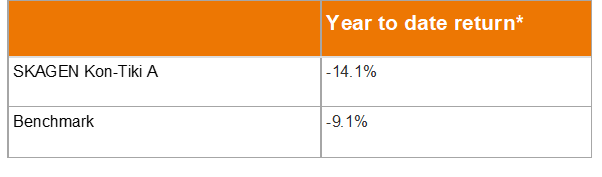

SKAGEN Kon-Tiki

- The fund's cyclical / energy exposure has been hard hit but the portfolio managers have added to their long-term conviction in Ivanhoe Mines as it is still in project build-out mode and has equity financing in place as well as strategic Chinese backing for whom it would make sense to buy out minorities at current levels.

- The portfolio managers have also added to Shell, given the attractive dividend yield (albeit not covered by cash flow), which they expect the company to maintain at all costs, including offering a discounted scrip dividend. With the large-cap energy companies having been amongst the hardest hit to date, the portfolio managers also expect their historical defensive characteristics to come into play as recession fears take hold in the wider economy.

- SKAGEN Kon-Tiki has maintained a 6% cash position through the sell-off, providing ample firepower for new opportunities. The team have used the drawdown to add three new positions that they have been monitoring for some time, which will be announced in due course. With valuations coming down significantly, they see an opportunity to test their hypotheses.

- The portfolio managers are working tirelessly to maintain the portfolio's highly attractive characteristics during a period of significant volatility and believe that they have a good balance between defensive assets (c 33% of portfolio has net cash position) and rebound potential.

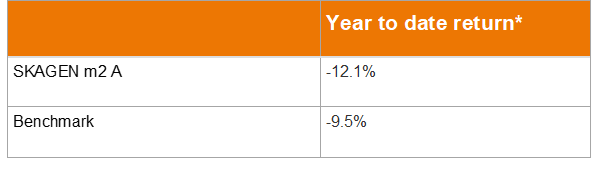

SKAGEN m2

- As expected, real estate continues to be more defensive than the broad index in downturns. However, it lags when the stock market turns and there is a surge as was the case in the US on Friday.

- The real estate market has initially acted very irrationally, probably driven by algorithms where some more resilient segments like self-storage, residential rental names and companies with long lease contracts (e.g. social infrastructure and data centres) were sold down as much as segments with short leasing contracts (e.g. hotels), which are correlated to economic growth (e.g. office) or are over-leveraged. This reverted during the week and investors started to behave more rationally again.

- SKAGEN m2 has had a hard time keeping up with the very US heavy benchmark due to its significant underweight. The US, which is not yet as affected by the virus outbreak, has cut interest rates and launched a number of major stimulus packages which are highly beneficial for the real estate sector. The Federal Reserve ramped up the amount of cash it is prepared to inject into funding markets over the next month, promising a cumulative total above USD 5 trillion, in a signal that officials will do whatever it takes to keep short-term financing rates from spiking.

- Europe, where m2 is overweight, is still in the eye of the Covid-19 storm. While the fund's underperformance could have been greater, it has benefited from the long-term strategy of investing a significant proportion of the portfolio in "defensive growth" names.

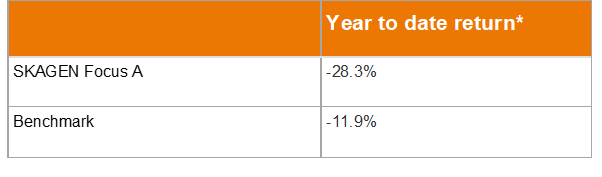

SKAGEN Focus

- The market sell-off has allowed the fund to establish several new positions in the US as stock prices move into the fund's price range, i.e. where 50% equity upside can be observed in 2-3 years on normalised earnings power. These include regional bank Citizens Financial, chicken producer Pilgrim's Pride and media company Disney. The portfolio managers are also closely monitoring several other potential assets in the US.

- The fund has further reduced the leverage risk factor across the portfolio, for example exiting the small position in ThyssenKrupp and also trimming the position in chemical producer Dow, which carries implicit energy exposure.

- The market correction has further stretched the polarisation between "cheap" and "expensive" stocks, illustrated by the value versus quality/growth gap. The portfolio managers strongly believe that the recovery, whenever it may come, will be led by the value stocks which are currently extremely cheap. This value opportunity is evidenced by the substantial 2-3 year upside potential across the portfolio.

- The fund's cash position is 7% which will be applied gradually into current and new positions on equity price weakness.

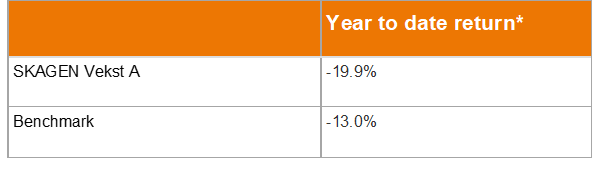

SKAGEN Vekst

- Oil companies have detracted most from the fund's performance, especially those with significant debt, but its telecoms exposure has helped stabilise the portfolio.

- The portfolio managers added to Bonheur and Yara. Bonheur is a completely different company today than it was during the financial crisis, given its exit from oil services and the cruise operating business is net cash. For Yara, first quarter results gave us increased conviction in the restructuring plan; the company has a strong balance sheet and earnings should be relatively insulated from the current environment (lower energy costs will be a positive in the short term).

- The portfolio managers reduced their position in Novo, as it increased to 9% of the portfolio. They also trimmed Samsung Electronics, and SK Telecom, which has held up well in the current environment.